By Brandon Perlow

The financial habits learned as a child or teen can last a lifetime. As such, financial literacy for children and teenagers is critical to economic success later in life.

A child with financial literacy has the knowledge and skills to effectively manage monetary resources, and that ability comes from financial education. A higher level of financial literacy for children and teenagers is associated with the following outcomes later in life:

- Less chance of using payday loans

- Lower-cost student loans

- Reduced likelihood of outstanding credit card balances

- Smaller private loan amounts

- Reduced delinquency and default

- Higher credit scores

As a parent, you play a crucial role in teaching your child about saving and managing money. If you’re unsure where to start, use the following primer on financial literacy for children and teenagers from the ABLE Financial Group to kick off the conversation.

Source: Fidelity

What Is Financial Literacy?

Financial literacy refers to the skills, knowledge, and confidence needed to make informed decisions regarding money. It requires a working understanding of concepts such as financial planning, debt management, and compound interest. Contrary to what many believe, these skills can be learned early in life. In fact, that’s the best time to impart them.

Why Compound Interest Is Key

Source: DaveRamsey.com

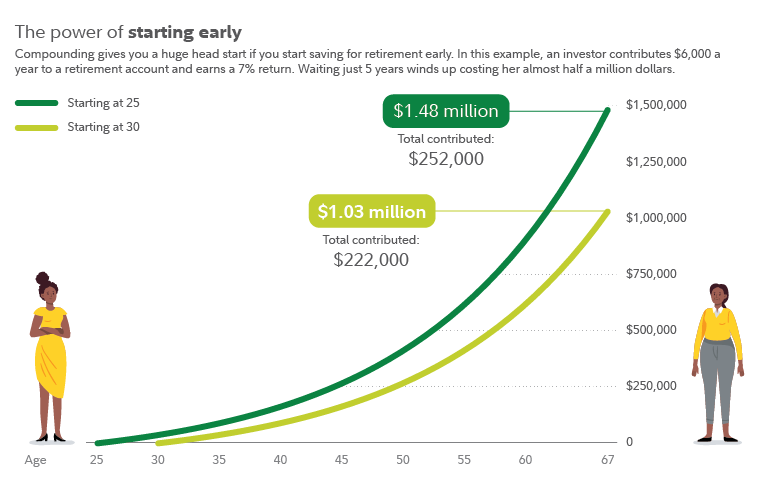

Saving early is one of the best gifts your younger self can give your adult self. Putting money away early in life allows your money to grow much more than if you begin saving later.

Consider the Rule of 72, which says that money tends to double by the quotient of dividing 72 by an expected rate of return. Assuming a rate of return of 8%, your money could double every nine years.

If you save $10,000 at 15, you could have $20,000 at 24, all the way up to $640,000 by age 69. But if you don’t start saving until 30, you’d only have $20,000 at age 39 and just $160,000 by 66. This example illustrates the all-important principle of compounding interest.

Source: Fidelity

Financial Literacy for Children and Teenagers: Best Practices

Depending on your children’s ages, some concepts may take longer to sink in than others. Here are some prudent steps to emphasize when discussing financial literacy for children and teenagers, even if they won’t apply for years to come.

Open a Roth IRA

In order to open a Roth IRA account, children must have earned income, so it’s a great idea if your teenager has a part-time job. For example, if your child earns $5,000 from mowing lawns, they could put it in a Roth IRA. However, you can further encourage saving by matching your child’s contributions. If your child contributes $2,500 to the Roth IRA, you and other family members could match that amount, rewarding your child and developing good savings habits. This money can grow tax-free and be withdrawn tax-free when your child turns 59½.

Contribute to a Custodial Account

A custodial account is typically a savings account opened and controlled by an adult on behalf of a minor. You can help your child fund this account by depositing their savings on their behalf, but you can also fund it with monetary gifts from you or even your parents—up to $18,000 annually or $36,000 from you and your spouse without using any of your lifetime gift tax exemption. The amounts are the same for your child’s grandparents.

You can use this account to teach your child about saving and investing even though the child can’t directly contribute to the account. For example, your child can pick a few companies that you could purchase shares of on their behalf—such as McDonald’s, Starbucks, Lululemon, Disney, Apple, Electronic Arts, or Nintendo. While the amounts invested don’t have to be great, this is a good way to help spark your child’s interest in finances and build their financial literacy.

Make Use of a High-Yield Savings Account

Keep cash in a high-yield savings account insured by the Federal Deposit Insurance Corporation (FDIC). Many accounts pay more than 5% interest, while banks only pay 0.01%–0.02% interest.

Manage Credit Responsibly

Adding your child as an authorized user on your credit card account can give them a head start to building good credit. Be sure to add their Social Security number when you add them as an authorized user. Different cards have different requirements, but generally this can be done once they are 13 years old. There are many free apps that can help young people learn to track their credit use. Using credit responsibly over time can lead to a higher credit score, which may qualify your child for lower interest rates for a mortgage or car loan down the road.

Consult a Financial Professional for Support

Are you interested in talking to a qualified financial advisor about financial literacy for children and teenagers? The skilled advisors at ABLE Financial Group can assist you in helping your kids plan for important life transitions.

To learn more about our team and the ways we can help guide you, call 480.258.6104 or email adam@ablefinancialgroup.com today.

About Brandon

Brandon Perlow has a diverse background, originally hailing from Buffalo Grove, Illinois. He graduated early in 2008 with a Bachelor of Science, double-majoring in Political Science and History, with honors, from the University of Wisconsin-Madison. Following this, in 2010, he earned a Master of Science in Public Policy & Administration from the London School of Economics, with merit.

Between 2010 and 2013, Brandon worked in the private equity sector in Los Angeles, California. From 2013 to 2017, he engaged in public speaking across the United States, focusing on topics related to student travel and cultural intelligence (CQ). Impressively, Brandon has extensive travel experience, having visited all 7 continents and all 50 states before the age of 25. In 2018, Brandon transitioned to the financial services industry in Arizona, concentrating on investment planning and retirement preparation. Holding AHIP Medicare Certification, he brings his experience and education to clients of ABLE Financial Group. He previously served as a Financial Advisor at both Merrill Lynch and Prudential Advisors in Scottsdale and Phoenix.

Beyond his professional pursuits, Brandon is passionate about volunteering. He currently serves on the Board of Directors for Gesher Disability Resources in Scottsdale and the University of Wisconsin Hillel Foundation. He is also on the Board of Directors for the Alumni & Friends of the London School of Economics in the United States. In the past, Brandon has contributed to various boards, including the City of Scottsdale Loss Trust Fund Board of Directors, the Real Estate & Finance Committee of the Jewish Federation of Greater Phoenix, and Business B’yachad at Temple Kol Ami.

In his spare time, Brandon is an avid runner, hiker, and adventurer. In 2021, he ran over 1,000 miles and served on the Pace Team for the Rock n Roll Arizona Marathon and Half Marathon in 2020, 2022, and 2023. He has achieved remarkable physical feats, including summiting Mt. Kilimanjaro, the tallest mountain in Africa, and completing the Rim-2-Rim hike at the Grand Canyon. Brandon resides in Scottsdale with his wife, Laurel, their daughter, Naomi, and their rescue Siberian Husky, Laney.